Posts from September 30th, 2022

Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

- 2026 | 12 Posts

- 2025 | 47 Posts

- 2024 | 39 Posts

- 2023 | 35 Posts

- 2022 | 58 Posts

- 2021 | 13 Posts

- 2020 | 25 Posts

- 2019 | 11 Posts

- 2018 | 1 Posts

- 2017 | 42 Posts

- 2016 | 66 Posts

- 2015 | 24 Posts

- 2014 | 64 Posts

- 2013 | 44 Posts

- 2012 | 38 Posts

- 2011 | 79 Posts

- 2010 | 38 Posts

- 2009 | 35 Posts

- 2008 | 1 Posts

30

Real Estate Slowdown Indicates a Healthy Housing Market

30

Sell Smart or Sell Fast? You Can Do Both!

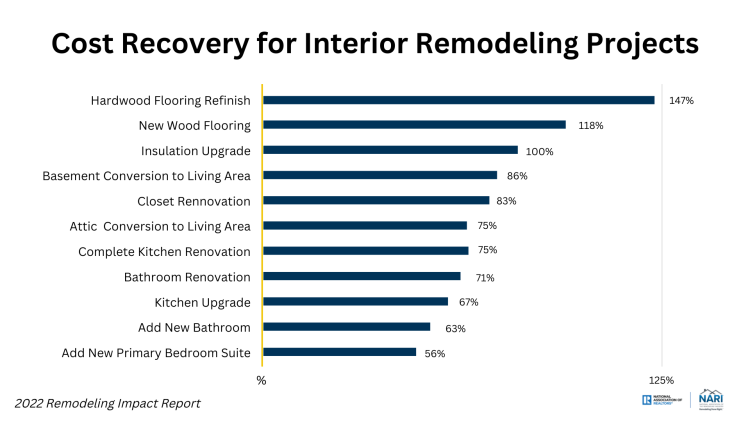

Earlier in the year, homes were selling at breakneck speeds. Freddie Mac reported that "Nearly two-in-five potential homebuyers would consider purchasing a home requiring renovations." With that kind of demand, home improvements took a back seat. However, today, the market is finding a new equilibrium - and so are sellers. Buyers have more options and can afford to be more selective. So now more than ever, sellers need to be smart about what renovations they choose to take on before listing their homes. Here is the latest data on cost recovery on remodeling projects for both interior and exterior remodeling projects.

Graph provided by the National Association of Realtors

30

What is Loan-to-Value (LTV) and Why is it Important?

By Chris Schneider, Vice President of Ruhl Mortgage The loan-to-value (LTV) ratio is a metric lenders use to measure the amount of debt used to buy a home compared to the value of the home being purchased. LTV is important because lenders use it when considering whether to approve a loan and/or what terms to offer. The higher the LTV, the higher the risk for the lender - if the borrower defaults, the lender is less likely to be able to recoup their money by selling the house.

What is LTV?

The loan-to-value ratio is a simple formula. (LOAN AMOUNT / HOME VALUE) * 100 = LTV% EXAMPLE: ($80,000 LOAN / $100,000 HOME VALUE) * 100 = 80% LTV Hint: This could also be considered in the reverse. For example, a borrower with 20% down payment has an LTV of 80%